How Your Credit Score Works in Canada — And the Mistakes That Are Costing Newcomers Their Mortgage

Every week I speak with clients who are confused about why their credit score is low. And more often than you'd think, the answer isn't what they expect. It's not because they missed payments or took on too much debt. It's because they did something that seemed responsible — like closing their credit cards — without realizing it would hurt them.

If you're new to Canada, this is not your fault. The Canadian credit system works differently than in many other countries, and nobody hands you a guide when you arrive. This post explains exactly how your credit score is calculated, what the most common mistakes are, and what you can do right now to start building a stronger financial profile.

What Is a Credit Score and Why Does It Matter?

In Canada, your credit score is a three-digit number that ranges from 300 to 900. The higher the number, the better. Most mortgage lenders want to see a minimum score of 620 to 680 for standard financing. The best rates and products are typically available to borrowers with scores above 720.

Your credit score is calculated by two main credit bureaus in Canada — Equifax and TransUnion. Lenders report your borrowing activity to these bureaus, and the bureaus use that information to generate your score. When you apply for a mortgage, your broker or lender pulls your credit report to assess how you've managed debt in the past.

A strong credit score tells lenders you are reliable. A weak score raises concerns — even if you have excellent income and savings. In the mortgage world, credit score is one of the first things a lender looks at, and it can mean the difference between being approved at a great rate or being declined entirely.

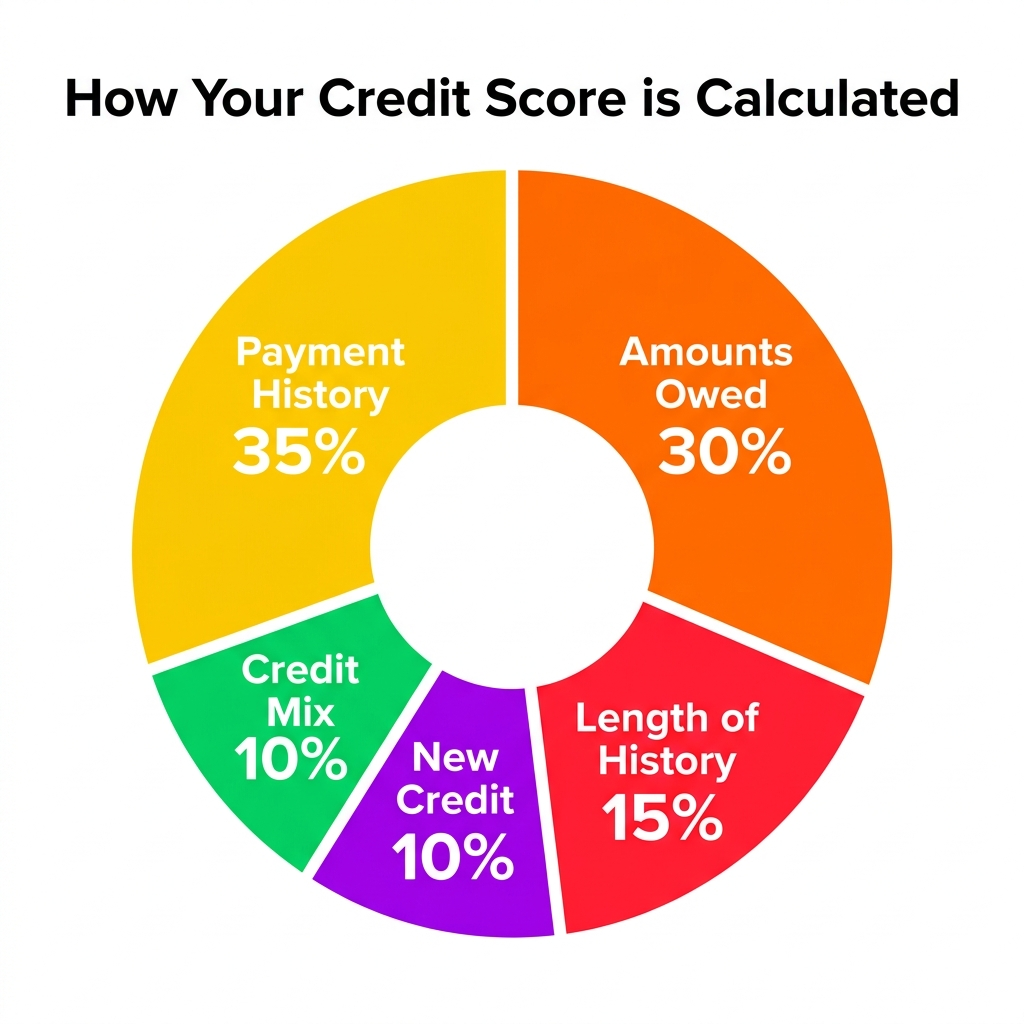

The 5 Factors That Make Up Your Credit Score

Your credit score is not random. It is calculated based on five specific factors, each weighted differently. Understanding these factors is the key to understanding how to improve your score.

1. Payment History — 35%

This is the single most important factor in your credit score. It measures whether you pay your bills on time. Every on-time payment strengthens your score. Every missed or late payment damages it — sometimes significantly.

The lesson here is simple: always pay at least the minimum payment on every account, every month, on time. Set up automatic payments if you need to. One missed payment can drop your score by 50 to 100 points and stays on your credit report for up to six years.

2. Amounts Owed (Credit Utilization) — 30%

This factor measures how much of your available credit you are currently using. It is called your credit utilization ratio. If you have a credit card with a $5,000 limit and you carry a $4,500 balance, your utilization is 90% — and that will hurt your score significantly.

The general rule is to keep your credit utilization below 30% of your available limit. So on a $5,000 card, try to keep your balance below $1,500. Even better, pay your balance in full each month.

This is also why closing a credit card hurts you. When you close a card, you lose that available credit limit. If you still carry balances on other cards, your utilization ratio goes up — even if your actual debt stayed the same.

3. Length of Credit History — 15%

This factor measures how long you have been using credit. The longer your history, the better. Lenders want to see a track record, not just recent activity.

This is one of the biggest challenges for newcomers to Canada. Even if you had excellent credit in your home country, that history typically does not transfer. You are starting from zero in the Canadian credit system. This is normal, and it can be overcome — but it takes time, which is why it is important to start building credit as soon as you arrive.

It is also why closing old accounts is so damaging. Your oldest accounts are your most valuable ones. Closing them shortens your average credit history and removes the foundation of your credit profile.

4. New Credit (Credit Inquiries) — 10%

Every time you apply for new credit — a credit card, a car loan, a line of credit — the lender performs what is called a hard inquiry on your credit report. Each hard inquiry causes a small, temporary drop in your score.

One or two inquiries in a year is normal and has minimal impact. But if you apply for five or six credit products in a short period, lenders may see this as a sign of financial desperation, and your score will drop accordingly.

The exception is mortgage shopping. If multiple lenders pull your credit within a short window (typically 14 to 45 days), credit bureaus often treat this as a single inquiry because they recognize you are comparing options, not desperately seeking credit.

5. Credit Mix — 10%

This factor looks at the variety of credit products you have. Having a mix of revolving credit (like credit cards and lines of credit) and installment credit (like car loans or personal loans) demonstrates that you can manage different types of debt responsibly.

You do not need to go out and acquire every type of credit product to improve this factor. It improves naturally over time as your credit profile grows. Focus on the bigger factors first.

The Most Common Mistakes Newcomers Make

After 16 years as a mortgage broker in Ontario, I have seen the same patterns repeat with clients who are new to Canada. These are the mistakes I see most often:

Closing credit cards to avoid temptation. I understand the logic — if the card is not there, you cannot overspend. But closing the card eliminates your credit limit, shortens your credit history, and raises your utilization ratio. All three hurt your score. A better approach is to keep the card open, use it for small regular purchases like groceries or gas, and pay the balance in full every month.

Never using credit at all. Some newcomers avoid credit entirely because debt feels risky. But in Canada, lenders need to see that you can manage credit responsibly. If you have no credit history, you have no score — and no score can be just as difficult to work with as a low score.

Applying for too many products at once. When people realize they need to build credit quickly, they sometimes apply for multiple credit cards at the same time. This triggers multiple hard inquiries and can actually lower the score they are trying to build.

Missing payments on small accounts. A single missed payment on a $200 store credit card can damage your score just as much as missing a payment on a large loan. Every account matters.

How Long Does It Take to Build or Rebuild Credit?

If you are starting from zero, it typically takes six to twelve months of responsible credit use to establish a score. From there, steady on-time payments and low utilization will continue to improve your score over time.

If you have damaged credit — missed payments, collections, or a consumer proposal — rebuilding typically takes one to three years depending on the severity and how actively you work on it. The negative items do not disappear immediately, but their impact fades as you build a positive track record on top of them.

Can You Still Get a Mortgage With Bruised or Limited Credit?

If your credit score is below the threshold for traditional bank financing, there are still options. Alternative lenders and private mortgage lenders evaluate your application differently, placing more weight on your down payment, income, and the property itself.

However, there is an important distinction to understand. Alternative lenders typically require a minimum of 20% down payment — sometimes more depending on the strength of your overall file. Private lenders may require even higher equity or down payment positions, often 25% or more, depending on the property, location, and the severity of the credit issues. These products also carry higher interest rates than conventional financing.

This means having savings matters as much as having a plan to fix your credit. If you are a newcomer or a buyer with bruised credit, building your down payment alongside your credit profile is the smartest dual strategy you can take.

That said, these products serve a real purpose. Many of my clients have used a short-term alternative or private mortgage to get into a property, spent one to two years rebuilding their credit, and then refinanced into a conventional mortgage at a much better rate. It is a legitimate and well-worn path to homeownership — but going in with accurate expectations is essential.

What You Can Do Right Now

If you are working on building or improving your credit, here are the steps that will have the greatest impact:

Never miss a payment — set up automatic minimum payments on every account so nothing slips through the cracks. Keep your credit card balances below 30% of your limit. Do not close old accounts — keep them open and use them occasionally. Avoid applying for multiple new credit products in a short period. Check your credit report at least once a year through Equifax or TransUnion to make sure there are no errors dragging your score down. Errors are more common than people think and disputing them is free.

Final Thoughts

The Canadian credit system rewards consistency and patience more than anything else. You do not need a perfect score to qualify for a mortgage — you need a score that reflects responsible financial behaviour over time.

If you are a newcomer to Canada, or if you have been through a financial setback that damaged your credit, the most important thing is to understand how the system works and take deliberate steps in the right direction. The sooner you start, the sooner your options open up.

I am Melissa Harney, a mortgage broker with 16 years of experience serving clients across the GTA, Durham Region, Dufferin County, and all of Ontario. If you have questions about your credit or want to know what mortgage options are available to you right now, I offer free consultations with no obligation.

Contact me at mortgagehubcanada.ca or call directly to get started.